Vietnam M&A: Momentum Meets Complexity

Seven signals shaping the next wave of deal activity — and the fault lines investors need to watch

Our perspective

Vietnam’s M&A market in 2025–2026 is defined less by volume than by intentionality. Whether domestic corporates restructuring balance sheets, regional platforms scaling capacity, global funds seeking contracted renewable yield, or impact investors building circular infrastructure — buyers are entering with clearer theses and longer holding horizons. For sellers and targets, this shifts the conversation: the right counterparty is increasingly one who brings strategic fit, not just capital. Navigating that match is where experienced advisory makes the difference.

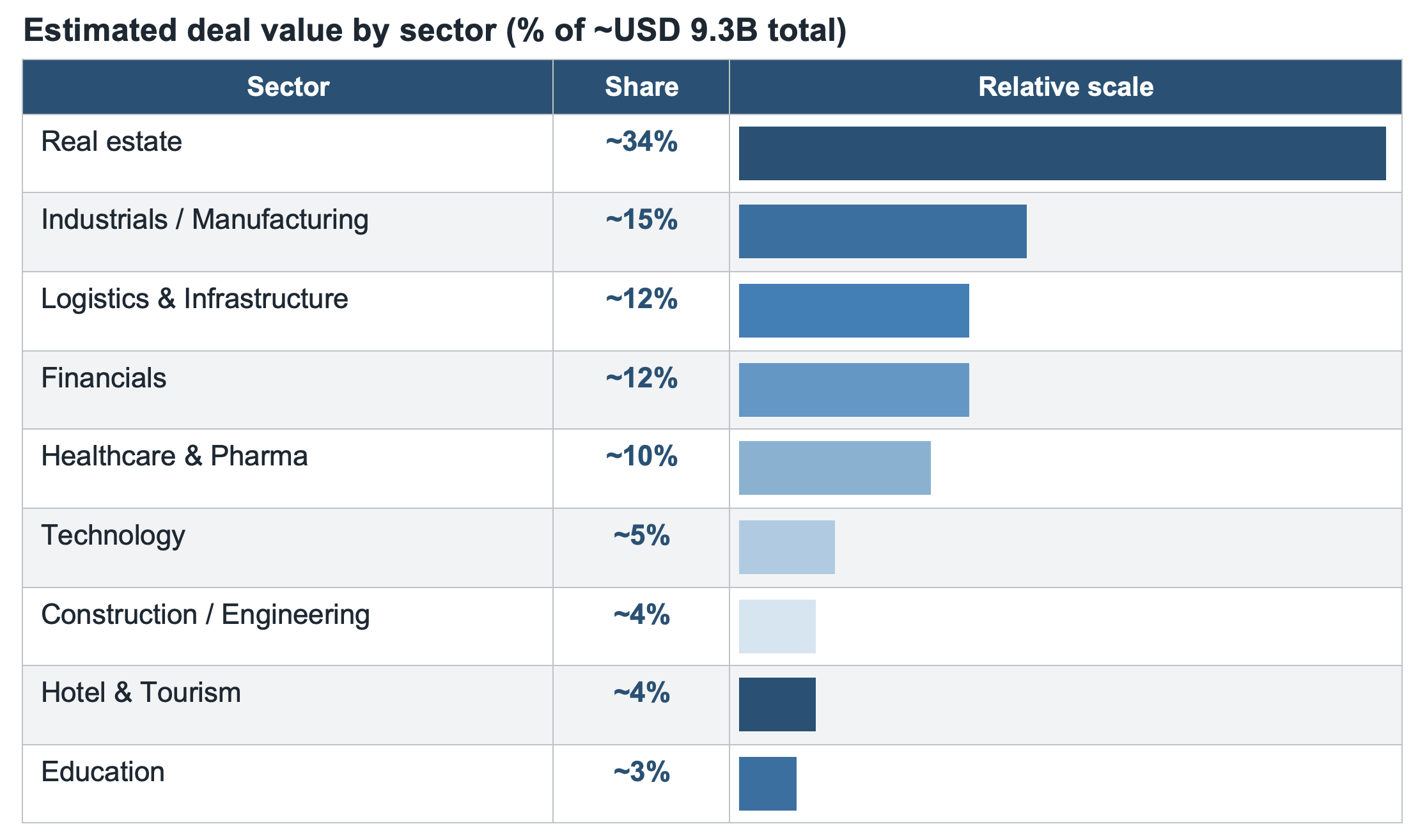

Vietnam’s M&A market has moved with conviction over the past fifteen months. With an estimated USD 9.3 billion in deal value across 2025 and early 2026 — spanning real estate, industrials, logistics, financials, healthcare, technology, and beyond — the market is no longer a story of potential. It is a story of execution. Below, we identify six themes that define where strategic and financial capital is flowing, and what they reveal about where the market is headed.

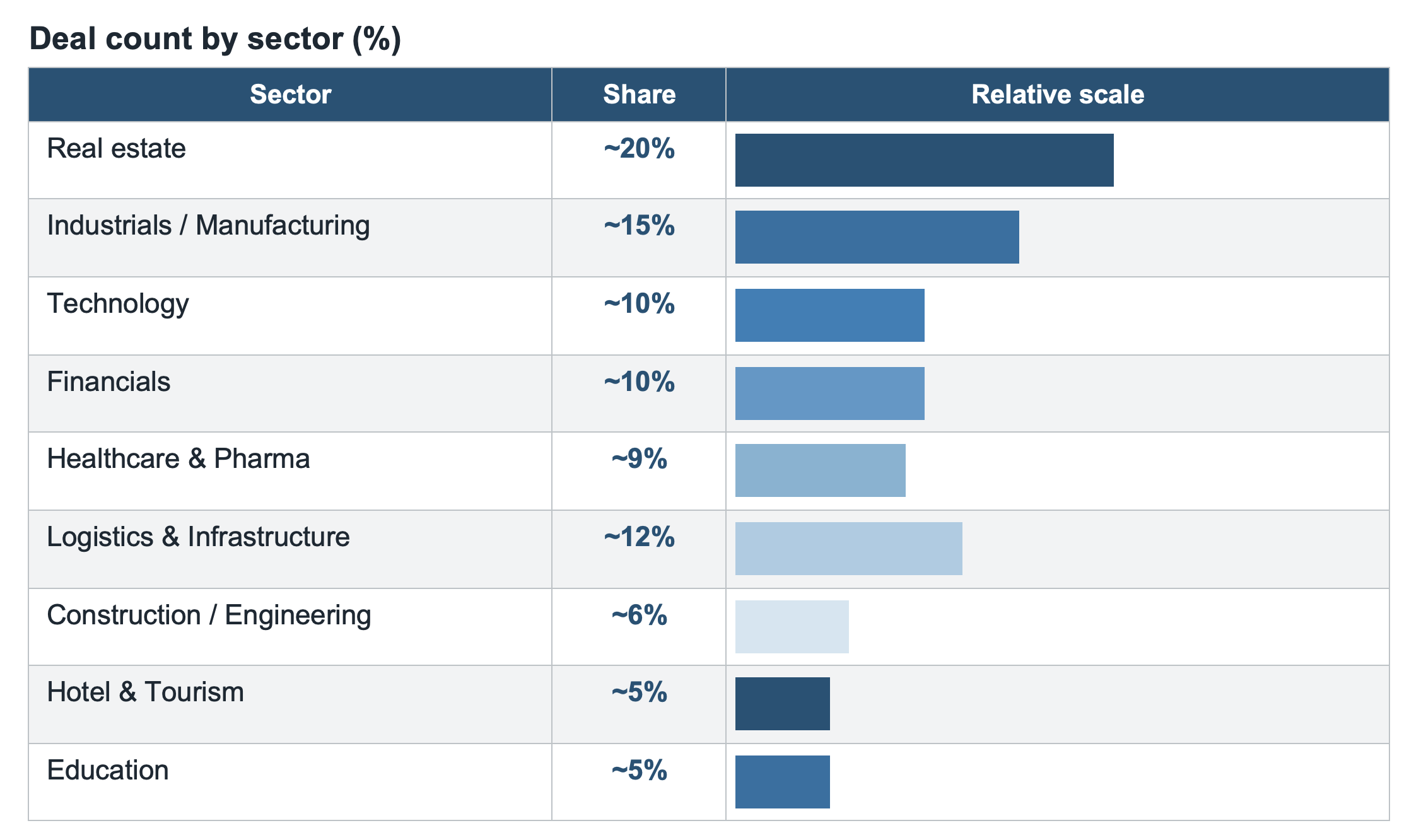

Market overview: deal activity by sector

The data below captures the spread of M&A activity across 2025–Q1 2026, showing both the number of transactions and their estimated value by sector. Real estate dominates by value; the spread of deal count across industrials, technology, and financials reflects the breadth of investor interest.

Seven themes defining the market

1. Real estate leads — but quality has replaced volume

At approximately 34% of total deal value, real estate remains the dominant sector. But investor selection is sharper than in prior cycles: both domestic and foreign buyers are prioritising assets with clear legal title and existing cash flows over development-stage plays.

Birch’s USD 365M acquisition of a controlling stake in Eastern Real Estate and the domestic-led USD 250–300M buyout of Vinaconex ITC — a divestment of non-core assets to restructure Vinaconex’s balance sheet — illustrate the same discipline from opposite ends of the capital table. FDI is returning selectively, prioritising cash-yield assets; domestic investors continue to lead where legal clarity exists.

2. Energy transition M&A is accelerating — brownfield is the entry point

Operating renewable assets with long-term power purchase agreements (PPAs) in place are attracting global energy transition funds at pace. Levanta Holding (backed by Actis) acquired 80% of HBRE Gia Lai Wind Power — a 50MW project in Gia Lai province with commercial operations since October 2021 and a long-term PPA with EVN — for USD 33.1M.

Gresham House (UK), via its SAETF fund, took 100% of Asia Clean Capital Vietnam (ACCV), which has developed and operated nearly 200MW of rooftop solar for industrial park clients since 2020. The pattern is consistent: platforms with contracted revenue are pricing well and transacting fast. Standalone development projects are a harder sell.

3. Logistics is consolidating — and converging with industrial real estate

Two forces are running in parallel. Global operators are deepening control: APM Terminals (AP Møller-Maersk) acquired a 49% operating stake in Hateco Hai Phong International Container Terminal — two berths at Lach Huyen capable of handling vessels up to 18,000 TEU — establishing direct gateway routes to the EU and North America. CJ Logistics completed its buyout of the remaining 49.1% of Gemadept Logistics Holding, moving from joint venture to wholly-owned subsidiary to fully integrate Vietnam into its regional network.

Simultaneously, domestic port players are expanding into land: Viconship acquired a 65% controlling stake (~VND 914 billion) in Harbour City, a company developing an industrial real estate project in Hai Phong’s Cat Bi Airport urban area. The line between port operator and industrial landlord is blurring.

4. Consumer finance: high conviction, high complexity

Consumer finance has attracted significant institutional capital — but the sector’s deal history in this period also highlights how quickly large transactions can unravel when due diligence and post-merger integration reveal gaps between disclosed and actual performance.

The AEON/PTF transaction is the most instructive case. AEON Financial (Japan) completed its USD ~166M acquisition of 100% of Post and Telecommunication Finance (PTF) from SeABank in February 2025. However, during post-merger integration, AEON discovered what it described as “inappropriate accounting transactions” in PTF’s pre-signing financial records. In June 2025, AEON formally notified SeABank that it considers the share transfer agreement invalid, demanded repayment and compensation, and stated it would pursue legal proceedings under Vietnamese law. SeABank has disputed the claim. The case remains unresolved and is a significant test of deal integrity standards in Vietnam’s financial sector M&A.

Market signal: The AEON/PTF dispute is a reminder that financial due diligence in Vietnam’s non-bank financial institution sector requires independent verification — not reliance on disclosed financials alone. Buyers with robust post-signing integration frameworks are better positioned to identify and act on discrepancies before they become legal disputes.

In a separate development, SCB (Thailand) formally terminated its planned ~USD 796M acquisition of Home Credit Vietnam after the conditions precedent under the agreement could not be met within the agreed timeline. Home Credit Vietnam — the second-largest consumer finance player in Vietnam with ~14% market share — remains unsold, and the outcome reinforces that regulatory timelines and deal conditions in Vietnam’s financial sector continue to present execution risk for large inbound transactions.

Against this backdrop, Kredivo Group (Indonesia) acquired Timo digital bank with plans to invest ~USD 15M over three years, retaining the Timo brand and integrating Kredivo’s BNPL and lending technology. The convergence of consumer credit and digital banking — using M&A to buy market entry — remains a live theme, even as headline deals face headwinds.

5. Healthcare attracts platform-building PE

Private equity is moving into healthcare with platform intent. Ares Management’s controlling stake acquisition in Medlatec Group (~USD 150M) is a build-out play aimed at scaling a private healthcare platform across Vietnam — not a short-term trade. Healthcare remains a high-conviction sector for PE, driven by structural underinvestment in private care infrastructure and Vietnam’s growing middle-class demand for quality medical services.

6. Foreign capital is returning — with a regional platform playbook

The common thread across inbound deals is regional scale ambition. SC Capital Partners (Singapore) acquired Serenity Holding — operator of the premium Fusion Hotel Group — with plans to integrate Fusion with HMJ (Japan) and Topotels (Indonesia), managing approximately 16,000 rooms across four high-growth Asian markets. Hoshizaki Vietnam increased its stake in ARICO to 99.62% to integrate ARICO’s manufacturing into Hoshizaki’s global supply chain.

These are not standalone Vietnam bets — they are nodes in broader regional strategies. Vietnam’s role as a manufacturing and hospitality hub within those strategies is growing, and the acquisition structures (full buyouts, near-100% stakes) reflect a preference for operational control over passive participation.

7. Impact and circular economy capital is entering — quietly, but meaningfully

Not every significant deal is measured in hundreds of millions. Norfund’s USD 4M equity investment into Circular Plastics Vietnam — via parent Circular Plastics International (Singapore) — to finance a recycling plant near Ho Chi Minh City signals a structural shift: impact and sustainable development capital is beginning to flow into Vietnam’s circular economy. The plant will expand capacity to 31,000 tons of PET flakes and 14,000 tons of food-grade rPET annually, serving both domestic and EU export markets.

As supply chain standards tighten and ESG requirements from global buyers intensify, this category of investment is likely to grow from a footnote into a theme in its own right.

DW Advisory

If you are evaluating a transaction or would like to discuss how these themes — or the risks they surface — apply to your strategy, we welcome the conversation. Please reach out to your DW contact or get in touch directly.