Power Law Distribution vs. Logistics Infrastructure: A Mathematical Impossibility

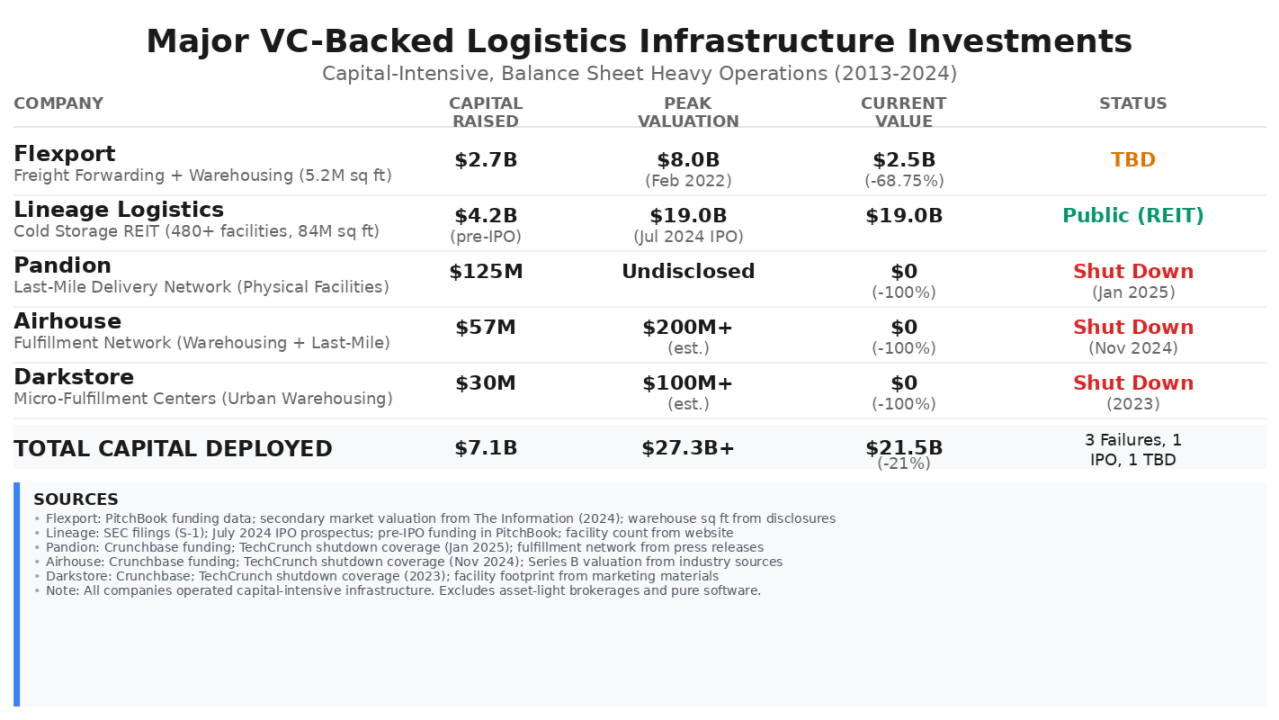

Major venture capital-backed logistics infrastructure investments from 2013-2024, showing capital raised, peak valuations, current values, and outcome

Late last week, I received my second call in three days regarding the feasibility of a freight brokerage roll-up centered around an artificial intelligence thesis. It was the eighth such call in the past year that I had received from a venture capital fund with 8 to 10-figure AUM. What was unique about last week’s calls was that both fund managers (the two largest I have spoken to date) had astutely identified a parallel of venture capital raised for Flexport, an infrastructure-intensive forwarder and transloader, as an argument for why a technology-based roll-up thesis of freight brokers wouldn't work as the capital intensity required to execute was high. (More about a multitude of AI-fueled brokerage roll-ups gaining steam in an article I'll publish in a couple of weeks.)

Both calls followed a familiar pattern of opening questions I had previously encountered as an icebreaker during semi-annual cadence calls with transportation and logistics MD's at the major investment banks: “Why is Stord one of VC’s most successful ventures in the supply chain?” or "Why did Convoy fail?" or, "Did you see Ryan Petersen's interview with Kramer on Mad Money?" The latter a testament to SBS Comms' exceptional work positioning Flexport's CEO across business media as a “subject matter expert” coupled with the inference most FINRA-regulated investment bankers think of Kramer more as an entertainment personality, than a credible analyst!

These conversations invariably circle back to the same fundamental question that the industry has been reluctant to answer directly: can venture capital and logistics infrastructure coexist? My answer, supported by a decade of empirical evidence and billions in deployed capital, is unequivocal: NO!

Comparison of Components and Characteristics of Logistics Infrastrcutre businesses

“Power Law Distribution” Meets 11% EBITDA Margins

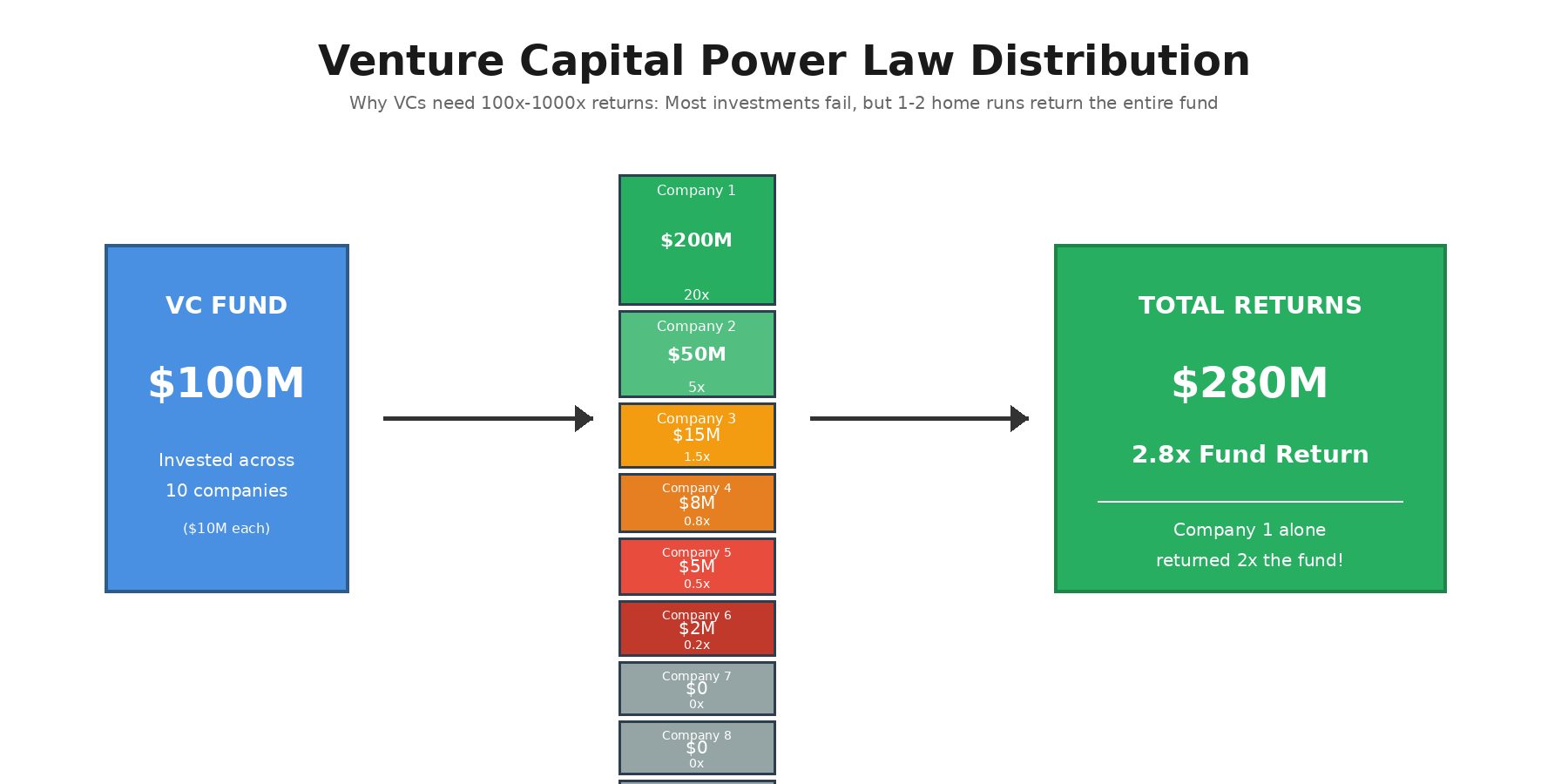

Venture capital operates on a power law distribution—a pattern where a tiny fraction of investments generate the vast majority of returns. In a typical VC fund, 1-2 "home run" companies might return the entire fund, while most investments fail or return modest amounts. This model requires the potential for massive, outlier outcomes: 100x or 1000x returns that can only come from high-margin, scalable businesses.

To understand why venture capital and logistics infrastructure are fundamentally incompatible, one can look at the few investments made, and of those, the failed report card. After a decade and over $20 billion invested, not a single venture-backed logistics infrastructure company has delivered the returns required. The math is deadly simple. Flexport's valuation collapse from an $8 billion peak, $2.5 billion in secondary markets and a 90% funding decline from 2021 to 2023 tell the story: VCs need 10x returns in 7 years, but logistics as an industry delivers 11% EBITDA margins and 7.4% ROIC (Return on Invested Capital). The survivors? Pure software companies like project44 and strategic asset-light infrastructure plays like Stord that avoided the fatal mistake of owning physical assets at venture scale. This isn't about execution failure, it's about mathematical impossibility.

Funds flow to illustrate "Power Law Distribution"

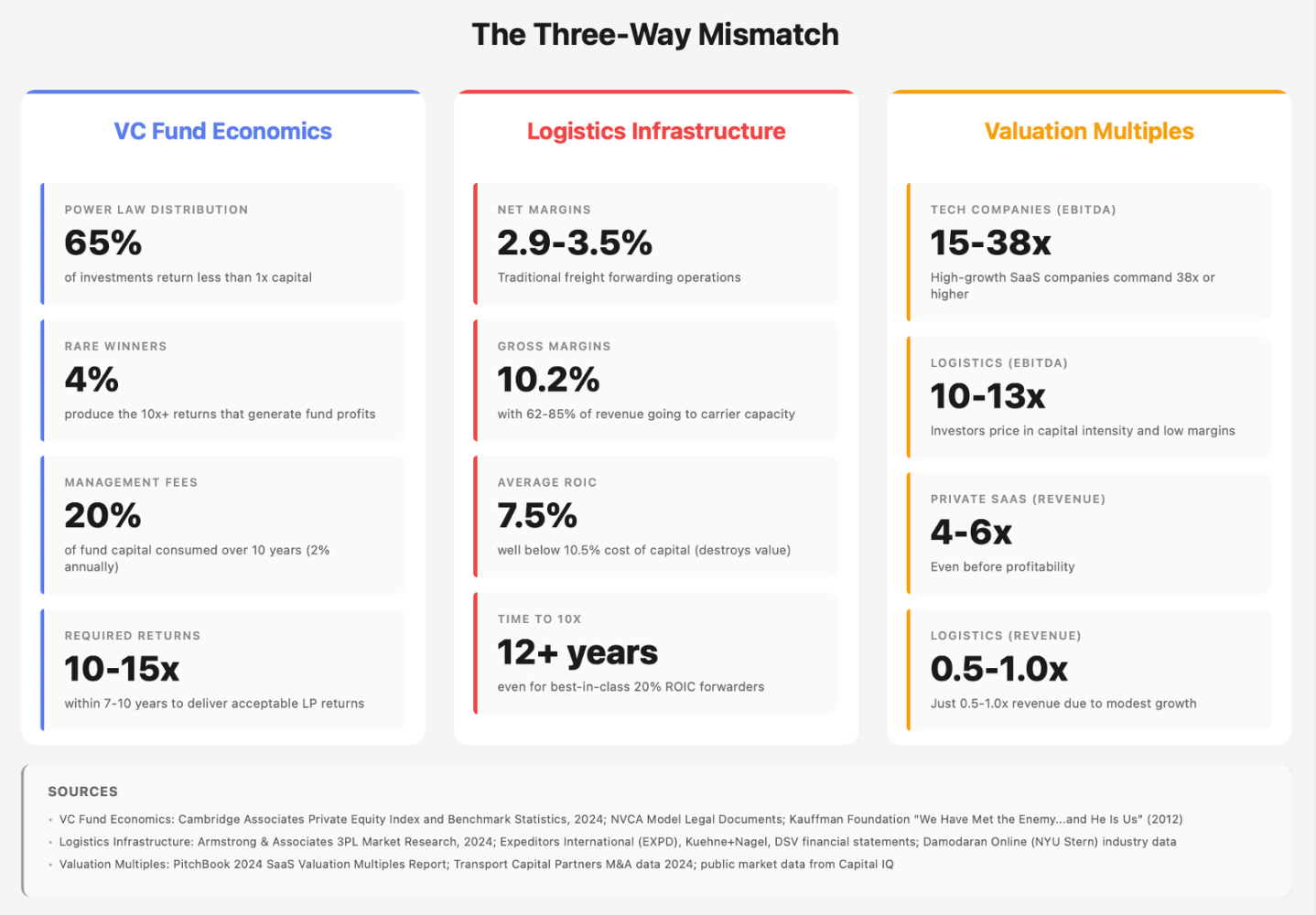

Fund Math Economics: Logistics vs Software

The fundamental incompatibility becomes clear when examining what venture capitalists actually need versus what logistics infrastructure can deliver. Power law distribution economics: 65% of investments return less than 1x capital, only 10% achieve 5x returns, and just 4% produce the 10x+ returns that generate most fund profits. This means successful investments must dramatically outperform to compensate for the majority that fail or return capital. After accounting for 2% annual management fees (consuming 20% of fund capital over 10 years) and the expected losses, VCs need individual winners to return 10-15x within 7-10 years just to deliver acceptable fund-level returns to their limited partners.

Now consider logistics infrastructure economics. Traditional freight forwarding operates at 2.9-3.5% net margins with 10.2% gross margins, while warehousing delivers 3-5% net margins, fulfillment centers operate at 2-4% net margins, transloading facilities generate 4-6% net margins, and asset-based trucking achieves 3-6% net margins—all capital-intensive, labor-heavy operations far removed from software economics. The largest cost component—purchasing carrier capacity in freight forwarding and brokerage—consumes 62-85% of revenue, leaving little room for the aggressive sales and marketing spend (often 40%+ of revenue) that venture-backed companies use to fuel growth. Warehousing faces similar constraints, with real estate, labor, and equipment consuming 75-85% of revenue, while trucking operations see driver compensation, fuel, and equipment maintenance absorbing 85-92% of revenue. Transportation and logistics companies generate 7.5% ROIC on average, well below their 10.5% cost of capital, meaning the sector destroys value rather than creating it on average. Even best-in-class freight forwarders with 20% ROIC face a mathematical problem: at 20% returns, doubling invested capital takes 3.6 years, and reaching 10x requires 12+ years—beyond VC fund lifecycles. Warehousing and fulfillment operations face even longer payback periods, with facility build-outs requiring 5-7 years to generate positive returns, while trucking equipment depreciates on 3-5 year cycles that prevent the exponential scaling venture investors demand.

Comparison of VC Fund Economics, Logistics Infrastructure Financial Metrics against Valuation Multiples

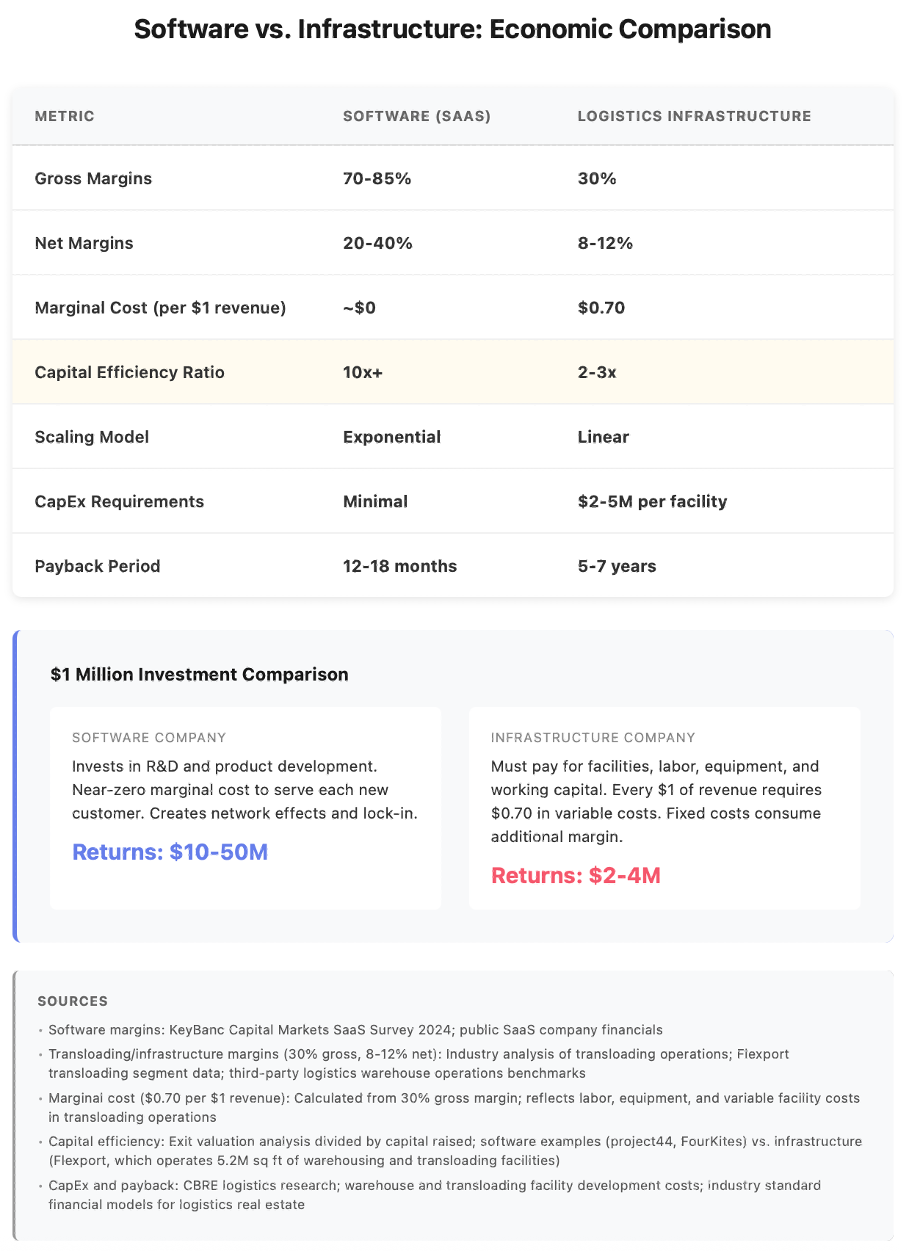

The contrast with software economics is stark. SaaS companies operate at 70-85% gross margins with near-zero marginal cost to serve additional customers. A $1 investment in software development can generate $10-50 in enterprise value through exponential scaling. project44 , the successful logistics software company, achieved $100 million+ ARR with 133% net revenue retention, meaning existing customers automatically expand spending over time. Meanwhile, in freight forwarding, every $1 of new revenue requires $0.70 in new costs (average of $0.62-$0.85) for carrier capacity, labor, and working capital. The business scales linearly, not exponentially, and offers no compounding revenue from existing customers.

The valuation multiple gap cements the incompatibility. Tech companies trade at 15-38x EBITDA in public markets, with high-growth SaaS companies commanding 38x or higher. Private SaaS acquisitions occur at 4-6x revenue even before profitability. Logistics companies trade at 8-10x EBITDA and just 0.5-1.0x revenue because investors rationally price in the capital intensity, low margins, and modest growth. This means even if Flexport hypothetically grew to match Kuehne+Nagel’s $31 billion revenue at 3% net margins ($930 million profit) and received a generous 1.0x revenue multiple, the company would be worth $31 billion. That's a respectable 11x return for early investors, but achieved over 13+ years, not the 7-10 VCs require. And this scenario assumes Flexport could achieve market leadership in a 130-year-old, highly competitive industry, an unlikely outcome.

CargoWise Closed the Technology Gap (nobody noticed)

The core narrative justifying Flexport's venture valuation was technology-driven disruption of "dinosaur" forwarders using "phones, fax machines, and paper." CEO Ryan Petersen frequently contrasted Flexport's modern software with competitors he described as "pre-GUI, like DOS, keyboard shortcuts only." The pitch implied that technology would enable better margins, faster growth, and a defensible moat justifying premium valuations. This narrative convinced SoftBank and others to invest billions at tech multiples for what is fundamentally a freight forwarding and transloading business.

CargoWise demolished this narrative, and barely anyone noticed. Developed by Australian company WiseTech Global , CargoWise is a comprehensive freight forwarding platform used by 96% of the top 25 global forwarders and 94% of the top 50 3PLs. The platform handles everything Flexport claimed as differentiation: real-time tracking, customs clearance across 195 countries, AI-powered document automation, multi-modal coordination, API integrations, and machine learning for optimization. WiseTech has delivered 5,800+ product enhancements in the last five years, invested $870 million in R&D, and maintains over 99% annual customer retention, retention rates that dwarf most software companies.

DHL Global Forwarding spent $1 billion trying to build internal technology before adopting CargoWise. Kuehne+Nagel, DSV, FedEx, Nippon Express, DB Schenker, CEVA, Aramex, and virtually every major forwarder completed global rollouts. To think that firms with over 10,000 professionals, deep industry expertise, and decades of operational knowledge wouldn't adapt to technological innovation is completely naive. These traditional competitors now operate on the same technology backbone Flexport claims as a differentiator, and they do it at a fraction of the cost. WiseTech's software-only business model generates 50% EBITDA margins selling subscriptions, while forwarders pay predictable fees without building technology themselves. The result: traditional forwarders achieved technological parity and can now process 2x the number of jobs per day compared to pre-CargoWise operations, giving them cost advantages to compete aggressively on price.

Consider the market dynamics: WiseTech Global commands over 40% market share in freight forwarding software with approximately $800 million in annual recurring revenue. Do you honestly think a firm with that level of market penetration and nearly a billion dollars in ARR wouldn't be obsessively listening to their customers and reinvesting capital to keep those clients competitive? The notion that incumbents would stand still while venture-backed startups disrupted them ignores basic survival instinct and competitive dynamics. WiseTech's continuous innovation, driven by direct customer feedback from the world's largest forwarders, ensures that the technology gap startup founders promise their investors simply cannot materialize.

UNIS employee demonstrating Apple Vision Pro technology integrated in Item.com platform

The incumbent adaptation extends beyond software platforms. Established infrastructure operators are now partnering directly with leading technology companies to drive efficiency gains that venture-backed logistics startups cannot match. UNIS is a leading privately held 3PL transloader backed by an expansive warehousing and real estate portfolio with strategic investments in innovation, including Cubework—the largest co-warehousing network—and Item.com, an advanced AI robotics system transforming logistics. The Walnut, California-based firm has partnered with Apple to deploy Vision Pro and Apple Watch technology in their warehouse operations, achieving double-digit efficiency improvements. This partnership demonstrates a critical reality: established technology leaders are choosing to work with proven infrastructure operators rather than backing venture-funded challengers. When Apple (one of the world's most sophisticated technology companies and second most valuable business globally) selects an established logistics operator like UNIS as its innovation partner, it signals that operational excellence combined with technology adoption beats pure-play venture models.

One digital forwarder executive admitted to The Loadstar: "Our platform is no different or superior to traditional forwarders with CargoWise." The gap that once existed between Flexport's technology and traditional offerings has narrowed so significantly that the "tech-enabled" label no longer justifies any valuation premium. Flexport's remaining advantages, a modern UI/UX, customer-facing dashboards, and supply chain data analytics are valuable but insufficient to overcome 3-10% margin disadvantages from higher cost structures. When Armstrong & Associates analyzed the landscape, their conclusion was blunt: "Legacy companies have invested heavily in automation, catching up" and now possess "a competitive advantage over pure-play digital freight brokers, especially those who have become overcommitted with too much venture or private-equity investment."

Spectacular Failure turned Resilient Pivot

The logistics venture capital graveyard tells a consistent story across multiple high-profile failures. Convoy raised $1.1 billion and reached a $3.8 billion valuation before shutting down in October 2023, citing a "massive freight recession and contraction in capital markets." Yet the core problem wasn't market timing. Digital freight brokerage still operates at 12-15% gross margins, and no amount of automation changes the fundamental requirement to compete on price in a commoditized market.

The irony runs deeper than most realize. On November 8, 2023, from my room at the 1 Hotel - Nashville on the night of the CMA Awards with cheers from the red carpet echoing through the room window, I demoed Transfix's technology stack that featured agentic AI built directly into their communication platforms, a full year before logistics "Vapi wrappers" began attracting eight-figure venture rounds. The platform was genuinely innovative, automating carrier communications, and freight matching with sophisticated AI that most competitors still cannot match.

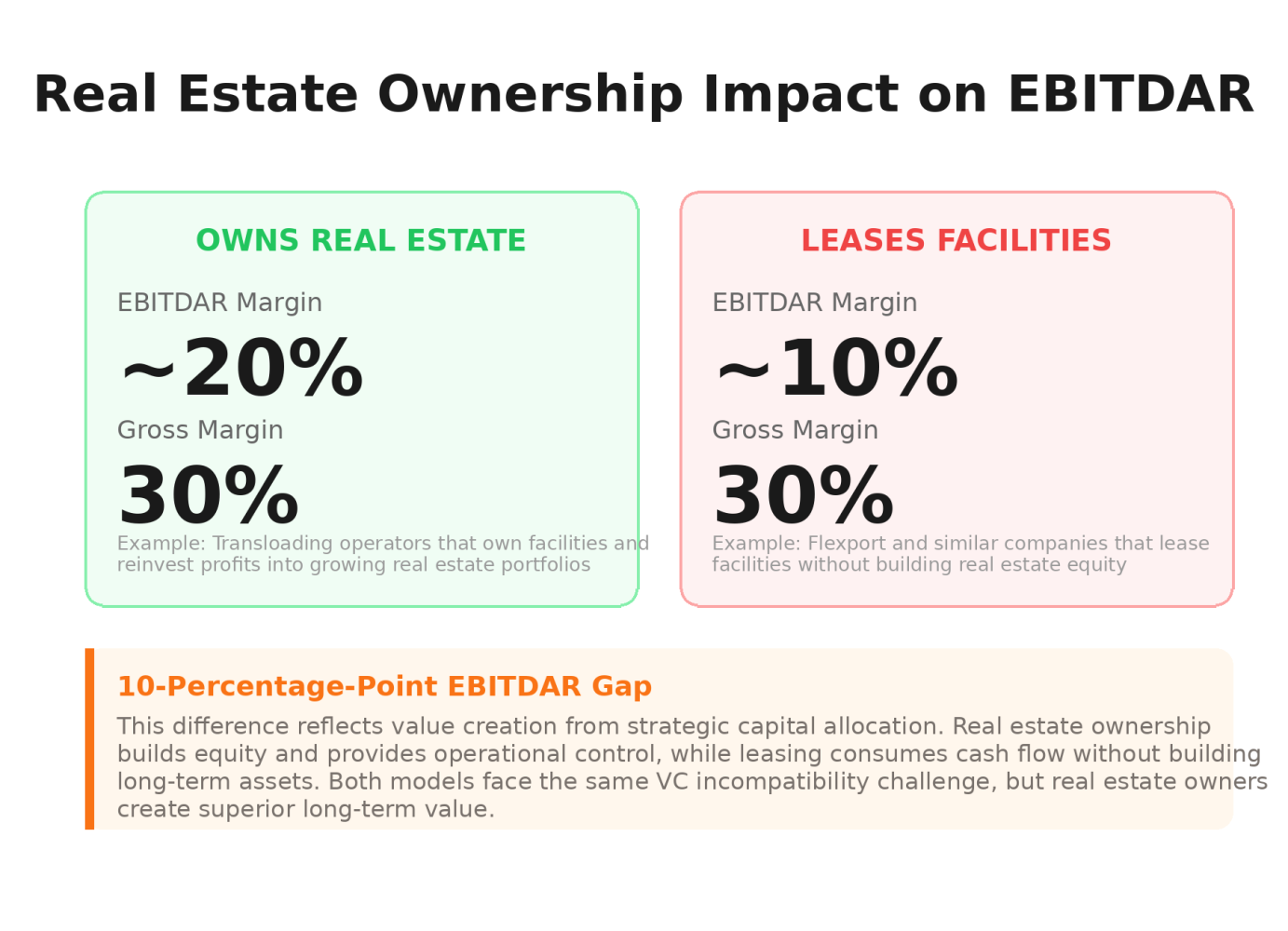

Comparison of EBITDAR Margins between logistics operators that own real estate versus those that lease facilities

When NFI acquired Transfix’s brokerage operations in June 2024, I realized they didn’t just acquire volume; they gained a technological edge over competitors, including well-funded ventures like Flexport. Transfix, a software solution that spun off its technology after selling its brokerage to NFI and gaining a prestigious inaugural client, is now cash flow positive, demonstrating that the technology proved effective when paired with adequate capital structure and operational discipline. Moreover, NFI, like UNIS , likely possesses a robust balance sheet of real estate assets accumulated over its 70 years in business, giving them a 10% advantage as real estate assets accumulate on the balance sheet compared to paying leases which is a sunk operating expense. Interestingly, the same investment firms that would later fund rudimentary voice AI implementations simultaneously cold-called me to assess broker roll-up theses, seemingly oblivious to the sophisticated technology already deployed by the companies they were evaluating. This disconnect highlights how venture capital’s fixation on buzzwords and pitch narratives often hinders investors from recognizing actual operational innovation occurring within established players.

Project44 and Stord: Playbooks that actually worked

Project44's success provides the counterpoint that proves the rule. The supply chain visibility platform raised $912 million across multiple rounds, reaching a $2.7 billion valuation, and actually achieved the growth and unit economics VCs require. The company tracks over 1 billion shipments annually for 1,300+ enterprise customers, generates $100 million+ in annual recurring revenue, and delivered 133% net revenue retention in 2021, meaning existing customers automatically expand their spending. The business operates at software margins (70-80% gross margins) because project44 doesn't move freight, own warehouses, or employ armies of operations staff. Instead, it provides API connections to carrier systems and processes tracking data, a true software platform that scales exponentially.

Stord represents perhaps the most instructive success story, a company that understood from inception how to leverage venture capital appropriately while respecting logistics economics. Rather than building physical infrastructure at venture scale, Stord created a software-enabled fulfillment network by partnering with existing warehouse operators, 3PLs, and freight forwarders. The company raised $330 million from Kleiner Perkins, Founders Fund, and Lineage Logistics itself, but deployed that capital primarily toward technology development and network orchestration, not warehouse acquisition. Stord's platform connects enterprise customers to vetted warehousing and transportation capacity without taking on the capital intensity of owning the assets. This model delivers software-like gross margins (40-50%) on fulfillment services while avoiding the working capital traps, real estate commitments, and labor management challenges that destroyed other ventures.

The critical distinction: Stord generates revenue by solving genuine pain points (complex multi-node fulfillment, inventory optimization, and carrier selection) through software, not by attempting to operate logistics infrastructure more efficiently than incumbents. When customers pay for Stord's services, they're primarily paying for intelligence, coordination, and integration capabilities that improve their existing operations. The physical movement of goods happens through Stord's partner network of established operators who already have the facilities, equipment, and operational expertise. This approach respects a fundamental truth: venture capital excels at funding technology development but fails catastrophically when applied to building capital-intensive infrastructure from scratch.

Both project44 founder Jett McCandless and Stord founders Sean Henry and Jacob Boudreau exemplify the "betting on the jockey" investment thesis. These humble, results-focused leaders prioritized customer outcomes over self-promotion, allowing them to navigate the delicate balance between venture capital expectations and operational realities. Their success validates that exceptional founders with industry expertise and measured approaches can deliver venture returns without compromising business fundamentals. These founders and their respective teams understood a fundamental principle: logistics needs better software, but that doesn't mean software companies should operate logistics businesses.

Economic comparison of software (SaaS) versus logistics infrastructure business models.

The economics explain why. Software companies can invest $1 million in product development and generate $10-20 million in high-margin revenue through exponential scaling. Every new customer costs almost nothing to serve, and successful products create network effects or lock-in that drives retention. Asset-light models also provide operational flexibility, shifting from CapEx (capital expenditures on fixed assets) to OpEx (operating expenses that scale with business), which dramatically reduces risk and improves capital efficiency. When you compare software capital efficiency ratios of 10x+ (exit value divided by capital raised) against logistics companies struggling to achieve even 1x, the distinction becomes obvious.

Meanwhile, every logistics infrastructure business fights the same battles: working capital grows linearly with revenue (you must pay carriers before customers pay you), labor costs resist automation beyond certain thresholds, real estate requires massive upfront investment with 5-7 year paybacks, and competitive dynamics force margin compression. Even supposed automation breakthroughs deliver modest improvements. Warehouse automation might reduce labor costs 20-40% but requires $2-5 million in upfront investment with multi-year payback periods. The dream of software-like margins in physical logistics operations remains exactly that: a dream contradicted by decades of industry data showing 2-4% net margins across economic cycles.

Lineage's REIT structure: Better Alignment, Same Hype Cycle

Lineage Logistics provides an instructive case study in both the promise and perils of infrastructure investing. The world's largest temperature-controlled warehouse REIT operates 480+ facilities with 84 million square feet across 19 countries. In July 2024, Lineage completed the largest real estate IPO ever, raising $4.4 billion at a $19 billion valuation. The company generates $5.3 billion in revenue with 24.9% EBITDA margins and pays investors a 5.3% dividend yield with steady, predictable growth.

Here's why the REIT model works structurally: REITs are legally required to distribute 90% of taxable income as dividends, forcing financial discipline that venture-backed companies lack. Investors accept 8-12% total returns (combining dividends and appreciation) rather than demanding 10x exits. The capital structure uses substantial debt (30-50% of assets) at 4-8% interest rates rather than expensive equity capital requiring 20%+ IRR. Most importantly, investor expectations align with business economics: slow, steady infrastructure development with modest but reliable returns, not hypergrowth.

However, Lineage itself was a product of the same capital abundance era that fueled Flexport. Lineage raised $1.9 billion in 2021, $1.6 billion in 2020, and $700 million in 2022 before the IPO, a blitzscaling exercise aimed at cornering the cold storage market through aggressive acquisition. This consolidation strategy has already spawned a new generation of cold storage infrastructure startups, suggesting that even the "right" capital structure can create market distortions when deployed with venture-style growth imperatives. The REIT structure provided better alignment than pure venture capital, but the aggressive expansion playbook came from the same hype cycle.

The valuation mechanics matter enormously. Lineage valued at 1.8x revenue on $5.32B as a REIT operating real assets is considered fairly priced. Flexport at 1.8x revenue ($3.8B valuation on $2.1B revenue) I would classify as overvalued because venture investors expect 10x+ returns. Both operate capital-intensive logistics infrastructure, but one used appropriate capital while the other didn't. The dividend requirement also forces operational excellence. You can't burn cash for growth when 90% of profits must go to shareholders. This discipline prevents the "growth at all costs" mentality that has destroyed numerous venture-backed logistics ventures.

Conclusion: Flexport’s Math Doesn’t Work

The Flexport story encapsulates everything wrong with venture-backing logistics infrastructure. Founded in 2013 as a "tech-enabled" freight forwarder, the company raised $2.7 billion from Softbank, Andreessen Horowitz, and other top-tier firms, reaching an $8 billion valuation in February 2022. By late 2024, that valuation had collapsed 52.5% to $3.8 billion. Secondary markets priced it even lower at $2.5 billion, representing a 68.75% decline from peak. The company executed four rounds of layoffs totaling over 1,600 employees, burned through hundreds of millions in cash, and missed its 2024 profitability target despite aggressive cost-cutting.

What makes this collapse instructive isn't execution failure—it's that even with world-class investors, talented leadership, and genuine technology innovation, the fundamental economics don't work. Flexport's business model combines freight forwarding (10% gross margins), customs brokerage, warehousing (5.2 million square feet it doesn’t own), and transloading (with higher 40% gross margins). All are capital-intensive, labor-heavy operations with 8%-12% net margins across business lines. When container rates spiked during the pandemic, revenue soared from $650 million in 2019 to $5 billion in 2022. But when rates normalized in 2023, revenue crashed 70% to $1.6 billion, exposing the business model's complete dependence on freight market cycles rather than any defensible "tech moat."

The company's financial trajectory reveals the core tension. In 2021, Flexport achieved its only profitable year with a 1.1% net margin on $3.3 billion in revenue, generating just $37 million in profit. That's $37 million of profit on a $2.7 billion capital base, representing a 1.4% return on invested capital. Traditional freight forwarders like Expeditors and Kuehne+Nagel operate at similar margins but use debt financing (4-8% cost) rather than venture equity requiring 30%+ IRR. For Flexport investors to achieve even a 3x return (well below the 10x VCs target), they would require a $24 billion exit valuation. At industry-standard 0.5-1.0x revenue multiples, that means growing to $24-48 billion in annual revenue while maintaining profitability. For context, Kuehne+Nagel, the world's largest freight forwarder after 130 years of operation, generated $31 billion in 2024 revenue.

The fundamental takeaway: software has value, but operating logistics infrastructure at venture-scale does not. Flexport’s math simply doesn’t compute.

The Future of VC Investment in Freight Tech

The logistics industry's VC experiment delivered one unambiguous lesson: venture capital is the wrong tool for infrastructure, regardless of how much "tech" rhetoric accompanies the pitch. The pattern of failures (Flexport, Pandion, Airhouse, Darkstore) represents not execution problems but model failures. These companies had talented founders, sophisticated investors, genuine technology innovation, and often years of operational experience. What they lacked was a business model capable of generating venture-scale returns from logistics infrastructure economics. VCs need 10x returns in 7-10 years, but logistics delivers 3% net margins (freight), 2-5% (warehousing/fulfillment), and 7.5% ROIC, well below the 10.5% cost of capital. The math proved it impossible, the graveyard proved it fatal, and the survivors proved that software (real, asset-light, high-margin software) was the only play that ever made sense.

The implications are clear. Software tools that enhance logistics operations remain excellent venture investments. Project44's success proves the model. But companies that own warehouses, operate fleets, employ thousands of logistics coordinators, or carry working capital for freight transactions should seek patient capital: debt facilities, private equity (conservative with leverage) with 3-7 year holds and operational improvement theses, strategic investors, or REIT structures with 8-12% return expectations that align with infrastructure economics. For founders, if your business model requires substantial physical assets or operates in low-margin logistics operations, VC funding will likely destroy your company even if it initially appears to help. The high burn rates, growth at all costs mentality, and exit pressure that come with venture backing are incompatible with businesses where margins cannot support aggressive expansion. For investors, the analysis demands honesty about return expectations matching asset characteristics. The multi-billion experiment proved that no amount of capital or technology rhetoric can overcome fundamental economic mismatches between venture requirements and infrastructure realities.

Most sophisticated VCs have already learned this lesson and stayed clear of logistics infrastructure investments. They see the empirical evidence confirming what many suspected: the fundamental economics simply don't align. It's not about execution, technology capabilities, or market timing. It's about whether venture capital's structural requirements can coexist with infrastructure economics. After a decade and billions deployed, we have an unequivocal answer. The question is whether the next generation of founders and investors will learn from this evidence before repeating the same expensive mistakes.

Written by

Want to know more?

Reach out to our team at Delta West Group to explore our full insights, including:

Venture Capital vs. Infrastructure Economics – Why power law returns are structurally incompatible with low-margin, capital-intensive logistics businesses.

Lessons from Flexport and Convoy – What recent high-profile failures reveal about the risks of applying VC models to freight.

Software-First Success Stories – How companies like project44 and Stord leveraged asset-light models to achieve venture-scale outcomes.

Alternative Capital Structures – How REITs, private equity, and strategic partnerships align better with logistics infrastructure economics.

Future of Freight Tech – Practical guidance for founders and investors on where innovation and capital can truly create value.